Northern NJ March Residential Sales

I have a hard time believing that I'm the fastest and most open source of New Jersey Real Estate News and Statistics. You would think with all the money that the NAR and NJAR have coming through the doors that they might have whole departments of analysts and economists releasing accurate and unbiased information on a regular manner.

A layperson would never have even seen this information. While the NAR and NJAR likely do have groups of people analyzing this data (one can hope), their intention is not to provide it to the public. Take the New Jersey Association of Realtors for example. They release their market reports quarterly, and it takes them months past quarter end to release them. By the time those reports hit the internet they are already stale, old news.

With that rant, here it is, the Northern NJ Real Estate Bubble Blog March Sales Analysis Report. By the public, for the public.

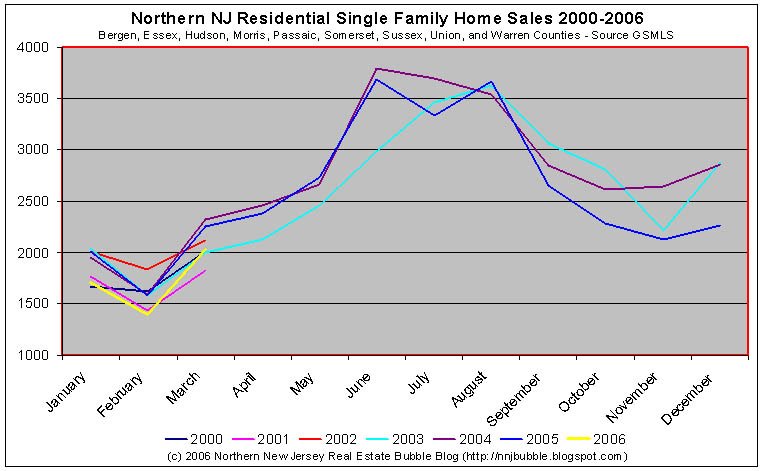

The first graph plots the unadjusted sales data (closed sales) for the counties listed. The graph isn't yet complete and is missing some historical data for 2000, 2001, and 2002. Please note the lower bound of the x-axis. It's set to 1000, not to zero. I do this for a reason, it's to emphasize the seasonal nature of the Northern NJ market. Also, there is quite a bit of data on this graph, setting the x-axis to zero makes reading it very difficult

A layperson would never have even seen this information. While the NAR and NJAR likely do have groups of people analyzing this data (one can hope), their intention is not to provide it to the public. Take the New Jersey Association of Realtors for example. They release their market reports quarterly, and it takes them months past quarter end to release them. By the time those reports hit the internet they are already stale, old news.

With that rant, here it is, the Northern NJ Real Estate Bubble Blog March Sales Analysis Report. By the public, for the public.

The first graph plots the unadjusted sales data (closed sales) for the counties listed. The graph isn't yet complete and is missing some historical data for 2000, 2001, and 2002. Please note the lower bound of the x-axis. It's set to 1000, not to zero. I do this for a reason, it's to emphasize the seasonal nature of the Northern NJ market. Also, there is quite a bit of data on this graph, setting the x-axis to zero makes reading it very difficult

The second graph displays the same sales data (2000-2006) for the first three months of the year. Again, please not the x-axis, this time it does cross at zero.

For those who prefer the hard numbers:

January

Median Sales (2000-2005): 1976

Average Sales (2000-2005): 1906

2006 Sales: 1705 (13.7% below Median, 10.5% below Average)

(2006 Sales were 15.3% below 2005)

February

Median Sales (2000-2005): 1586

Average Sales (2000-2005): 1607

2006 Sales: 1395 (12.1% below Median, 13.2% below Average)

(2006 Sales were 11.6% below 2005)

March

Median Sales (2000-2005): 2060

Average Sales (2000-2005): 2087

2006 Sales: 2033 (1.3% below Median, 2.6% below Average)

(2006 Sales were 9.9% below 2005)

Caveat Emptor!

Grim

50 Comments:

Grim,

Where did you get this data from?

If the bubble is bursting, why is the spread between '05 and '06 sales narrowing?

What am I missing?

Data is provided to me by real estate professionals who have direct access to the MLS systems.

I have made a number of contacts over the past 6 months who have committed themselves to providing me this data as well as other 'insider' information about what is going on at their local offices.

grim

grim:

to quote Kramer relative to your work

"ahhhh - the mother lode"

thank you [etc. etc. etc.]

Richard,

I'm not sure what you mean by surge. While we're closely following the behavior seen in 2004 and 2005, we're doing so at approximately 10% below the levels seen during those years. I might agree with you if what you mean is that seasonal trends seem to have shifted between 2000-2003 and 2004-2006.

Sales were higher in March, but then again, sales are always higher in March.

On an absolute level, sales in last month were lower than March sales last year and the year prior.

I'd never trust my own memory to make a call like that.

grim:

OK - you upped the bar and I appropriately genuflect.

Now that the formalities are over.

You gave us numbers, but what is your opinion?

I'll throw this one out - where do we draw the line for "dead as a doornail" under 1500 for a March? Obviously, all the years in the sample are strong - roughly 2K.

How many more TOTAL single family home are there in the sample from 2000-2006 [new construction etc.]?

Is it possible that you are missing closing data from earlier years?

Is the market still have legs?

Is this pent up demand that will burn off?

Do you think that supply numbers [if they they were ever ascertainable] would give more of a complete story?

Do I sound as if I am trying to make up excuses for putting a negative spin on what is clear at worst neutral data?

Others' opinions?

chicago

I've said this in another thread. Since 70% of households are owners, what percentage of the other 30% are actively looking or waiting?(How many could qualify once stndards tighten up?)

Since we saw that over 40% of sales last year were fo investment and second homes, where does that demand end. Was that done mostly with ARM, IO.

The market sentiment has changed which I think will dry up investor demand. As foreclosures increase on ARM and IO FB's I think there will be a huge slump in the RE market. Anybody else got an opinion on the 30% market that are not owners?

it's cleary a downward trend as the numbers state and the graphs show...

chicago finance said

"Do I sound as if I am trying to make up excuses for putting a negative spin on what is clear at worst neutral data?"

not at all...

br

grim,

What happened to your friend at the Star Ledger that mentioned you in her article. Has she been writing any more. Would she do a write up on some of this data?

I think that the upward bounce in March might be due to people looking in that warm January and finally closing in March. Just a guess.

Skep-tic,

I would wager that if that was the bounce it might have been the result of people not clued in to the market. I believe that April will look more like 2000 or late 90's (or lower) as more people get a clue.

i'm first time buyer looking around north jersey, and getting really disheartened by what's available...my wife and i combined make over 125K/year, yet somehow can only afford newark/irvington! ok, that's a bit of an exaggeration, but there's slim pickens in the low 300s elsewhere in north jersey. even if list prices come down, it seems taxes and interest are up up up, so it's really a no-win situation. maybe i'll soon be one of those statistics of houng professionals leaving NJ...

while i'd like to admit publicly that i'm hung, that should actually read "young professionals..." up there.

Rentinginnj

I think 30% is close to the historical average. Historically, most of these people either prefer to rent or simply don’t have the means to buy.......

Actually 70% home ownership has never happened before in the U.S. Ever! So my point is that 30% population is an interesting cohort.

Just me speculating. But I think the market has almost been tapped out in many areas. In NJ generally the more urban your home is the more likely you rent. And conversely the more rural the more likely you own. Sussex for example had close to 80% ownership in the 2000 census.

RentinginNJ:

That's absolutely correct, the graph does not show a function of supply and demand.

Could the bounce be a reflection of some price drops?

Interesting posts.

Am I correct, these figures are SINGLE FAMILY homes (i.e. no condos)?

If you reflected supply of condos - the numbers would go through the roof.

Also, with March - I assume that we are referring to actual "closes" not accepted offers.

As a result, a strong March is actually reflective of the massive Wall Street bonuses paid in January and people with money burning a hole in their pockets. January was also extremely warm as I recall.

Although grim documented all of the mess in the last few weeks, these anecdotes won't be reflected until April's and May's numbers.

Am I good a rationalization or what? :-)

Here's some data I just got for Hillsdale, in order by date sold:

MLS: 2505549

401 Kinderkamack Rd

OLP $525,000

Sold 7/22/05 $525,000 DOM 71

MLS 2510562

32 Riverdale St

OLP $589,900

Sold 7/28/05 $606,000 DOM 16

2.73 % above asking

MLS 2518081

OLP $689,900

Sold 8/23/05 $704,000 DOM 6

2.04 % above asking

MLS 2526340

29 Morris Dr

OLP $539,900

Sold 9/5/05 $562,000 DOM 12

4.09 % above asking

MLS 2525510

122 Knickerbocker Ave

OLP $549,900

Sold 11/15/05 $566,000 DOM 58

2.93 % above asking

MLS 2533901

52 Morris Dr

OLP $649,000

Sold 12/15/05 $660,000 DOM 9

1.69 % above asking

MLS 2534023

227 Piermont Ave

OLP $569,000

Sold 1/11/06 $562,500 DOM 29

1.14% Lowball

MLS 2529106

71 Holdrum St

OLP $699,000

Sold 2/7/06 $730,000 DOM 54

Note: Owner had NJ RE License!

4.43 % above asking

MLS: 2600996

141 Riverdale St

OLP $520,000

Sold 2/28/06 $530,000 DOM 28

1.92% above asking

MLS 2536613

266 Magnolia Ave

OLP $619,900

Sold 3/1/06 $585,000 DOM 70

5.63% Lowball!

MLS 2533113

55 Standish Rd

OLP $610,000

Sold 3/21/06 $535,000 DOM 83

12.3% Lowball

Grim-

Great charts...I would love to see supply and avg. prices plotted against this. That would be the classic supply and demand economic model as someone mentioned above. I have to believe supply is rising versus previous years based on some of the numbers you keep posting.

JM

One other thought, I wonder if there is any way to get data on how many of these were pre-foreclosure and/or investment properties?

Skep-tic,

I meant 70% nationally. Do you know if that stat is actual based on banking data or estimated like the census does with much of it's data between deccenial censuses?

Maybe a chart of average days on market would be helpful?

Here are some inventory numbers for various towns I follow (Grim, is it possible to you allow the PRE tag on blogger?).

Short Hills, 07078

Date / Total / Under 1M

2-Mar-06 94 12

3-Mar-06 93 15

7-Mar-06 93 16

14-Mar-06 97 15

16-Mar-06 101 13

21-Mar-06 105 13

30-Mar-06 108 15

6-Apr-06 115 18

Millburn, 07041

Date / Total / Under 1M

3-Mar-06 18 15

7-Mar-06 17 14

16-Mar-06 22 18

21-Mar-06 21 16

30-Mar-06 15 11

6-Apr-06 20 14

Summit, 07901

Date / Total / Under 1M

3-Mar-06 67 25

7-Mar-06 72 29

16-Mar-06 75 31

30-Mar-06 80 29

6-Apr-06 85 35

Chatham, 07928

Date / Total / Under 750K

3-Mar-06 85 15

8-Mar-06 87 17

14-Mar-06 93 20

21-Mar-06 89 19

30-Mar-06 104 28

6-Apr-06 111 28

Don't be a debt slave to your mortgage. The one's benefitting from your misfortune are the same ones that are telling you go ahead sign the paper and get a risky loan.

DO NOT DO IT.

YOU WILL BE GRATEFUL YOU DIDN'T AS THE HOUSING MARKETS PROGESSES INTO A BUST.

Delford makes an interesting observation about our senior citizens. I noticed this myself in local town stores over lunch that there are a lot of people of retirement age in my local area. It is a little morbid,and please I love and respect our older generation as much as anyone, but as they downsize, move into assisted care facilities, etc this will only add to the inventory. Granted this demographic shift is occurring over many years but I couldn't help noticing how many seniors we have locally (and good for them, that they are able to get out and about.)

"Hey, you young whippersnapper! You can't get me out of my house. I built this in a blizzard with a handsaw, bailing wire, and a mallet! So, go take your new fangled blogger thing somewhere else"

Okay, sorry just had to get that in...I agree the demographic shift is hitting right as the RE market is downturning. And, don't forget, many people are expecting their homes to be their retirement funds. Should get interesting...

Data is GSMLS only and is SFH, Condos and Coops.

There are a few issues to keep in mind.

This represents sales via one MLS system only. This doesn't include NJMLS, MLSGuide, or non-MLS sales.

This is important when comparing historical trends due to the fact that market share may have shifted. However, looking at the data, that doesn't appear to be the case, but keep that in mind.

grim

Interesting price drop in Hoboken here.

http://www.hobokenx.com/html/modules/newbb/viewtopic.php?topic_id=1806&forum=9

Demographically speaking, the oldest Boomers will turn 60 this year, and the youngest will turn 42. There are many more boomers than there were Post-War babies, the youngest of whom will turn 61-78 this year.

Unless there are large numbers of boomers retiring early (which hasn't been the case so far) I wouldn't expect to see a decline in demand strictly because of age-related reasons.

There are tons of younger boomers still out there who could ostensibly fill the "void" left by seniors.

Here's a random thought-

Thinking about seniors...is it possible that many of them live in lower-priced homes given that older homes tend to be much smaller than newer construction homes? If, as others suggested, seniors move out of SFRs and into other housing will a larger number of homes suitable for first-time buyers become available?

I know I've read that the median prices may have risen because there is a dearth of starter homes on the market...could this change that?

It could make home ownership more of a reality for our "houng" professionals in NJ! :-)

Just a thought...

My opinion?

I'm still waiting for a trigger.

We've had two events take place that are plausable explanations, the increase in ARM rates and a change in psychology (how the heck do you quantify that, anyone want to be a pollster?).

The increase in ARM rates is a good explanation for the drop off we've seen in sales.

The shift in psychology is a good explanation for the increase in inventory. I suppose everyone could have just decided they wanted to sell now, but it seems unlikely.

So we've got some correlations, but causation is based entirely on assumption.

We're in the very early stages of the cycle. I agree with the analogy mentioned before, we're at the apex of the arc.

grim

Here's a quick walk thru (I'll be making a lot of assumptions about proportions, but based on reasonable amount of knowledge)of the potential impact of baby boomers on a national level (don't know NJ particulars):

- 75 million+, let's say 1/2 born 1946-1956, so roughly 38 million are 50+

- of those 38 million, let's take as a guesstimate 50% to get the HH # = 19 million

- 19 million X 50% have/had over 2 kids and needed at least 3 bedroom SFH/Condo = 9.5 million HH 3 or more bedroom homes

- Now, the first wave of this group has already had kids leave home and go to and graduate from college. I'll guess half, so 4.75 million HH with at least one kid gone.

- Or, say 10% (10 yrs/10) or .95 million will be eligible to receive SS in 2008.

Ok, now take those two in half (a lot of people won't want to downsize or retire right away) .475 and 2.388 million, I think that's the range of houses that will flood the market nationally in 2008. That would represent somewhere between around 10 and over 30% of the total home sales this year. That's huge! Alright, let the theory hole punching begin.

JM

skep-tic said...

whichever way you slice it, the demographic trends don't favor real estate, esp big suburban homes.......

I have seen speculation that these monster houses may becom multifamily in the future.

Jeffrey Otteau who does market analysis for real estate professionals, bankers and appraisers had this to say about the current market:

If you're looking for a positive sign in the New Jersey housing market you can take some comfort in knowing that increase in contract-sales activity from December to January was slightly greater than the month-to-month increase of 1 year ago. Despite relative improvement however, sales activity in January ran 12% less than January 2005 indicating that the weakness in the residential market which began in October has carried over into 2006. Further evidence that the market has softened comes from the continuing increase of unsold inventory which grew by more than 2,000 homes in January and now stands 46% higher than 1 year ago. Home buyers will clearly have much more to say in determining the selling price of a home in 2006 than was the case last year.

Despite these signs, the Spring Market will arrive, although later than we've grown accustomed to in recent years. Look for the Spring rally to start in late March once home buyers realize that the long predicted collapse in housing prices won't occur and as climbing mortgage interest rates bring some urgency back into the home buying equation.

With all the increased competition on the market this year, the appearance of a home will play a greater role in determining marketing success. Items such as condition, décor, and curb appeal will take on greater significance

as home buyers have a wider selection of competing homes from which to choose.

skep-tic,

i don't know about that... i think that late spring bounce call just might be correct... now, don't get me wrong... i truly believe that we are in a bubble... but there are people who don't care about price and are just willing to buy... and that's ok... just watch the inventory... that will tell you where the market is moving... good luck to all!

Another link for piece Skeptic mentions at CNN

http://tinyurl.com/huawj

Just my opinion... but another driver that could give this market a late spring bounce is that the fed and the OCC are still in the process of tightening up the lax lending standards... those stated mortgages do have a higher interest rate but they are still available... and it's going to take months for the fed and the OCC to pass and then enforce their new guidance rules... so... the real question is, are there enough buyers to sustain this particular market? does it have legs? we'll see... again... i believe the real indicator is the inventory.

www.HomePriceMaps.com/cherryhill.htm integrates how much homes SOLD for in Cherry Hill as well as nationwide using the google mapping technology. If you don't see data for your area simply email HomePriceMaps@gmail.com with your zipcode and or address and they'll update the site and email you within a few days.

Payroll growth is steady at a clip that is well in excess of population growth. As a result, the labor market is tightening. The wage number actually decelerated a bit in March, but the Fed can not be comfortable with the pace at which the labor market is moving to/through full employment. We are not anywhere close to the 1999/2000 labor market tightness, but we are certainly moving in that direction. While these data do not change our read of the economy, they strike yet another blow to the popular mantra that "the economy is about to slow."

-- Stephen Stanley, RBS Greenwich Capital

The wage increase in today's report was below expectations and will not in itself set off alarm bells. But with the unemployment rate edging down again, the Fed will remain concerned about tightening "resource utilization." The overall picture -- robust growth with some threat of higher inflation -- suggests that the Fed will raise interest rates at least two more notches to 5.25% by the end of June.

-- Nigel Gault, Global Insight

Meager wage growth combined with a falling unemployment rate will keep investors asking questions about the "resource utilization" justification for future FOMC rate hikes, despite a very strong household survey combined with an on-consensus establishment survey. However, we continue to believe that the unemployment rate is an important factor in wage growth.

-- Drew Matus, Lehman Brothers

Growth in employment was well entrenched in the first quarter. Strengthening wage gains and increased hours worked pushed our proxy for wage income up 6.8% in the first quarter at an annual rate, which is the fastest increase since the second quarter of 1999. The Fed is likely to be concerned about the continued tightening of labor markets, which should keep the Fed on track for at least two more rate hikes. This report underscores the self-sustaining nature of the recovery with broad based job gains and firming income trends.

-- John Ryding, Conrad DeQuadros, Elena Volovelsky of Bear Stearns

The household survey also showed a surprisingly elevated reading for "not at work due to bad weather" -- one of our favorite proxies for weather-related influences on the payroll data. The March reading of 250,000 was a good deal higher than is typical for that particular month and even matched that seen in February, despite the fact that a significant blizzard battered the East Coast right around the February survey period (note: keep in mind that this series, unlike all the key data in this report, is not seasonally adjusted). So, if conditions turn more normal in April, we could see some weather-related upside.

-- David Greenlaw and Ted Wieseman, Morgan Stanley

The details largely reinforce perceptions of the relative pace of activity across sectors. Though construction employment rose just 7,000, the strong increases the two prior months keep job growth in this sector on a solid trajectory. With the hurricane-rebuilding efforts still not in full swing, construction employment could continue to rise even as the expected slowdown in home-building takes hold.

-- David Resler and Gerald Zukowski, Nomura Securities International

Today's jobs report confirms 5% Fed Funds in one month. If next month's report looks the same in terms of strength, you can book 5.25% as well. The report is too strong. The Fed is going to react.

Next meetings 5/10; 6/28; 8/8 - you really have to starting thinking that 5.50% is at least a 30% shot at this point.

Fix out those mortgages!

The Ten is at 4.98%

Just my opinion... but don't count on the default rate of I/Os and other types of ARMs to bring this market down... that's not what this is all about... this is about what types of mortgage products are available to the marginal homebuyer... if the fed and OCC drag their feet for months, which is what looks like is happening, then most likely 2007 will be the year for a serious sea change.

Grim out sick today? (Friday)

Skep-tic said...

The rapidly rising house prices come at a time when the baby boomers are moving out of their years of peak housing demand.

FWIW, historically people age in place. They lay down roots have friends etc. So moving out is not that likely (even with rising taxes). The story here is that according to a demographic expert I saw at a conference last year, she said we will see boomers upgrade there housing and not downsize.

Grim,

Awesome data. No wonder they don't share this openly on the net.

Delford,

I'm just repeating what the "expert" said. I was surprised and don't completetly agree.

Also as for the upgrade, in alot of the RE ads I've seen alot of it involve amenity based communities, i.e. golf, tennis, etc. for them to semiretire with.

Not sick, but away from a computer. Was hanging around with the Wall Street crowd this morning.

grim

Here is a quote from moneycentral.msn.com from today:

"...The greatest risk to bonds right now, in my opinion, is that the new chairman of the Federal Reserve won’t be as adroit as the old. Ben Bernanke is possibly more of an inflation hawk than Alan Greenspan was, meaning it will be tempting for him to drag us all into a recession by hiking rates too high for too long."

If that happened we might see much greater and more rapid decline in home prices. 40% and even more would not be unrealistic.

Grim,

Is it possible to compare the residential inventories vs. sales between '05 and '06.

Thanks.

I have been following a site now for almost 2 years and I have found it to be both reliable and profitable. They post daily and their stock trades have been beating

the indexes easily.

Take a look at Wallstreetwinnersonline.com

RickJ

I have been following a site now for almost 2 years and I have found it to be both reliable and profitable. They post daily and their stock trades have been beating

the indexes easily.

Take a look at Wallstreetwinnersonline.com

RickJ

Blogging is a hit or miss trip ... usually a miss ... but I did enjoy reading your blog, which I put in the 'hit' category. Thanks for look. Stop by my site if you can.

Post a Comment

<< Home