New Jersey Economy To Slow

From the APP:

Anemic economy forecast for N.J.

Rising unemployment, a slowdown in the housing market and declining business for vendors could add up to an anemic economy for New Jersey in the coming months, according to the latest data from the Federal Reserve Bank of Philadelphia.

The regional bank's latest forecast for the Garden State, issued Friday, pegs economic growth through early next year at just 0.4 percent, a precipitous drop from the bank's last two forecasts of modest growth.

Economist Ted Crone, a vice president at the bank, said the drop "could be just a little blip."

"I would want to have a couple more months' data before we go out onto a limb" by predicting much slower growth, he said.

The prior two forecasts were for economic growth of 1.8 percent and then 1.4 percent, each over the subsequent nine months, but both were later revised. The most recent forecast, for example, was cut from 2.2 percent growth to 1.4 percent, and the 0.4 percent estimate could be revised later.

The data used for the latest forecast, collected in April, include the biggest jump in the state unemployment rate in more than three years, Crone said, from a 4.5 percent rate in March to 5.1 percent in April — the highest level in two years.

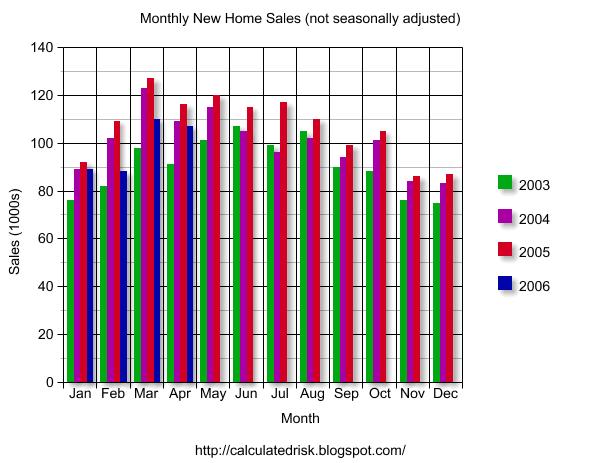

Meanwhile, vendors surveyed by the bank reported getting raw materials and goods to customers quicker, a sign they had less business to handle, and the number of new-home construction permits dropped from about 2,240 in March to 1,660 in April. Crone said the market for both new and existing homes has been slowing nationwide as well as in New Jersey, with prices increasing less rapidly and the inventory of unsold homes rising.

"We don't expect a total collapse. It's just like letting a little air out" of the once-hot market, he said.

Anemic economy forecast for N.J.

Rising unemployment, a slowdown in the housing market and declining business for vendors could add up to an anemic economy for New Jersey in the coming months, according to the latest data from the Federal Reserve Bank of Philadelphia.

The regional bank's latest forecast for the Garden State, issued Friday, pegs economic growth through early next year at just 0.4 percent, a precipitous drop from the bank's last two forecasts of modest growth.

Economist Ted Crone, a vice president at the bank, said the drop "could be just a little blip."

"I would want to have a couple more months' data before we go out onto a limb" by predicting much slower growth, he said.

The prior two forecasts were for economic growth of 1.8 percent and then 1.4 percent, each over the subsequent nine months, but both were later revised. The most recent forecast, for example, was cut from 2.2 percent growth to 1.4 percent, and the 0.4 percent estimate could be revised later.

The data used for the latest forecast, collected in April, include the biggest jump in the state unemployment rate in more than three years, Crone said, from a 4.5 percent rate in March to 5.1 percent in April — the highest level in two years.

Meanwhile, vendors surveyed by the bank reported getting raw materials and goods to customers quicker, a sign they had less business to handle, and the number of new-home construction permits dropped from about 2,240 in March to 1,660 in April. Crone said the market for both new and existing homes has been slowing nationwide as well as in New Jersey, with prices increasing less rapidly and the inventory of unsold homes rising.

"We don't expect a total collapse. It's just like letting a little air out" of the once-hot market, he said.

posted by grim

19 comments

![]()

![]()