"Bubbles do burst"

Economist Robert Shiller, of Irrational Exhuberance fame, gave a rather important interview to ABC/Nightline news yesterday. I say important because it means the housing bubble is beginning to get significant exposure and coverage in the mainstream news.

Robert Shiller, the Prophet of House Prices

Economics Professor Predicted the Dot-Com Bust; Sees Another on the Horizon

If a prophet is only as good as his last prophecy, then you'd be wise to listen to Robert Shiller. On "Nightline," Shiller offered his considerable analysis of the current real estate market … and he doesn't bring good news.

It was back in the heady stock market days of 1996 that Shiller, an economics professor at Yale University, gave voice to his first prophecy. He warned that the stock market was overheating and that investment had risen to what he described as irrational levels. The stock market crash that followed was no surprise to Shiller and proved that he had called it right.

Now he's warning that a similar collapse may soon apply to the real estate market. And there's evidence that he may be right here, too.

...

Shiller argued that human emotion, not strategic economic factors, drives prices and property buying.

He argues that many first-time buyers pay inflated prices simply because they fear they'll be left behind...

Shiller has traced the actual financial return that houses produce for their owners. He says that over the long term, house prices roughly match gains in people's incomes and that booms are more often followed by busts, thereby dissipating any major increases in equity.

----

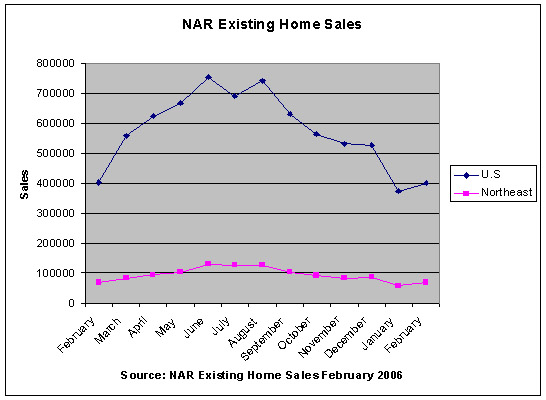

The Star Ledger ran an AP piece on the New Home Sales report today:

New home sales plunge 10.5 percent

New home sales fell the biggest amount in al most nine years in February while home prices declined for a fourth straight month, raising concerns the once high-flying housing market could be in for a rougher-than- expected landing.

...

Analysts, who had been forecasting a much more moderate drop of around 2 percent in February sales, said the big decline and downward revisions to sales activity in the previous three months could be signaling that housing will slow more this year than had been expected. "The new home market looks like it is starting to stagger," said Joel Naroff, chief economist at Naroff Economic Advisers, a Pennsylvania forecasting firm. "Bubbles do burst."

Caveat Emptor!

Grim

Robert Shiller, the Prophet of House Prices

Economics Professor Predicted the Dot-Com Bust; Sees Another on the Horizon

If a prophet is only as good as his last prophecy, then you'd be wise to listen to Robert Shiller. On "Nightline," Shiller offered his considerable analysis of the current real estate market … and he doesn't bring good news.

It was back in the heady stock market days of 1996 that Shiller, an economics professor at Yale University, gave voice to his first prophecy. He warned that the stock market was overheating and that investment had risen to what he described as irrational levels. The stock market crash that followed was no surprise to Shiller and proved that he had called it right.

Now he's warning that a similar collapse may soon apply to the real estate market. And there's evidence that he may be right here, too.

...

Shiller argued that human emotion, not strategic economic factors, drives prices and property buying.

He argues that many first-time buyers pay inflated prices simply because they fear they'll be left behind...

Shiller has traced the actual financial return that houses produce for their owners. He says that over the long term, house prices roughly match gains in people's incomes and that booms are more often followed by busts, thereby dissipating any major increases in equity.

----

The Star Ledger ran an AP piece on the New Home Sales report today:

New home sales plunge 10.5 percent

New home sales fell the biggest amount in al most nine years in February while home prices declined for a fourth straight month, raising concerns the once high-flying housing market could be in for a rougher-than- expected landing.

...

Analysts, who had been forecasting a much more moderate drop of around 2 percent in February sales, said the big decline and downward revisions to sales activity in the previous three months could be signaling that housing will slow more this year than had been expected. "The new home market looks like it is starting to stagger," said Joel Naroff, chief economist at Naroff Economic Advisers, a Pennsylvania forecasting firm. "Bubbles do burst."

Caveat Emptor!

Grim

posted by grim

9 comments

![]()

![]()