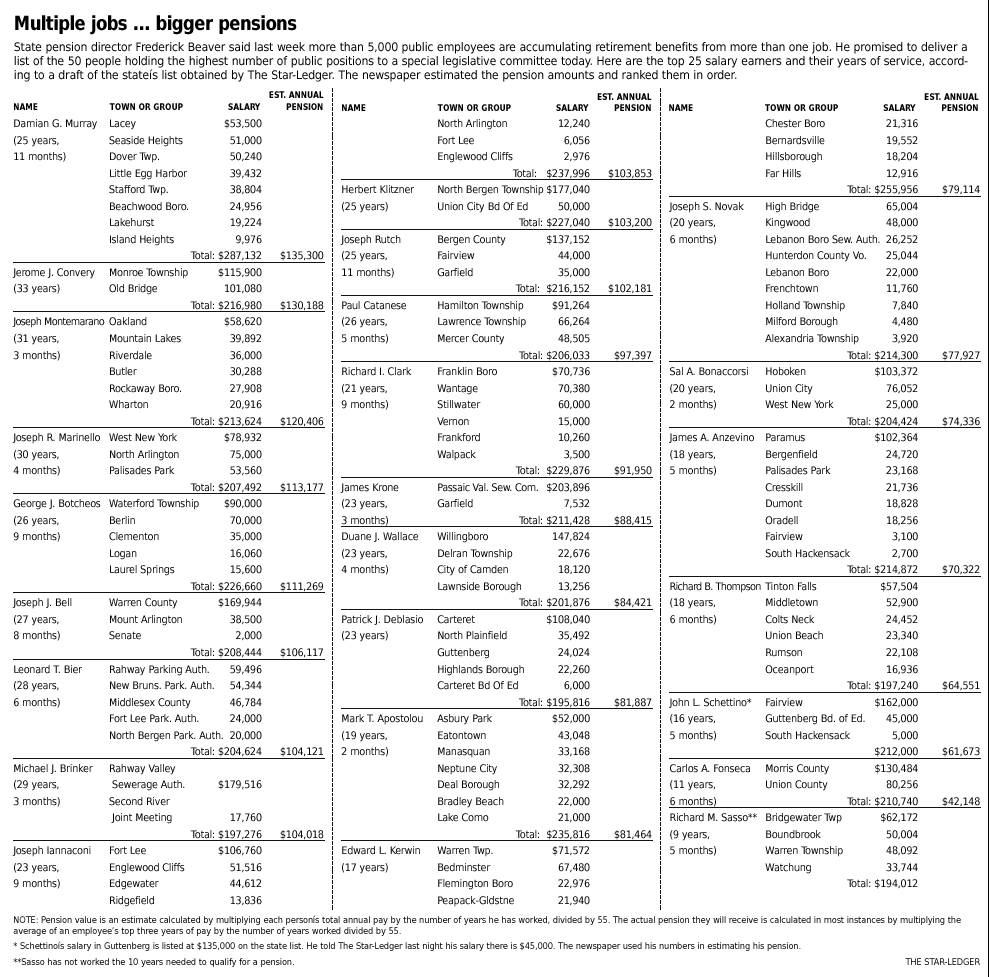

The End Of Real Estate As We Know It?

From the New York Times:

The Last Stand of the 6-Percenters?

The Last Stand of the 6-Percenters?

Redfin and other innovators, including ZipRealty and BuySideInc.com, are using technology to reduce costs and to save time for their brokers. Agents don’t find and recommend homes — customers do that on their own, using Internet listings — and that enables agents to charge less for the services they do provide, chiefly handling the paperwork and negotiations.

The Internet has radically changed the way consumers buy books and airline tickets, trade stock and learn news. But the real estate industry has resisted change — and protected its commission structure — by controlling the information on its Multiple Listing Service database of properties for sale.

“You can find out more on the Internet about an eBay Beanie Baby than you can about a $1 million house,” said Glenn Kelman, chief executive of Redfin, a licensed broker in Washington State and California.

...

Traditional agents still firmly control the M.L.S., which allows all participating brokers, including Redfin, to view almost every home for sale in a particular area, even those being offered through competitors’ agencies. But the typical 6 percent commission, paid out of the seller’s proceeds and split between the seller’s and buyer’s agents, is under attack because, as economists note, it does not serve consumers well.

...

In many cities, real estate agents have tried to restrict access to M.L.S. information or to limit its use on the database. Some have asked state legislatures to pass laws forcing brokers to offer certain levels of service, a move that Mr. Kelman sees as intended to squeeze out discount brokers. “It’s a thousand tiny shackles on innovation,” he said.

...

The Justice Department and the Federal Trade Commission have fought these tactics in Texas, Kentucky, Tennessee and Oklahoma, among other states, and the department is suing the National Association of Realtors, the powerful trade group of agents and brokers, over what it calls anticompetitive rules.

“Where it comes to our attention that significantly anticompetitive state laws or regulations are under consideration, we approach state officials to advocate that they take into account the benefits to consumers of a more competitive approach,” said J. Bruce McDonald, deputy assistant attorney general for the antitrust division of the Justice Department.

...

Buyers also enter details of their offers — the price they want to pay, the size of the deposit they are willing to put up and, for example, whether they will pay for the termite inspection. Then they click on “Submit.” A Redfin agent checks everything with the customer before passing along the offer to the seller.

“It took eight minutes,” said Perry Webster of Des Moines, a suburb of Seattle, who bought a new four-bedroom house through Redfin. “But it didn’t really matter that it was online. We just liked the business model.” He asked, “Is it really worth $10,000 to ride in a real estate agent’s Lexus?”

posted by grim

9 comments

![]()

![]()